If you just won the Virginia Mega Millions, your first instinct is to scream, celebrate, and call your family. But the single most important thing you can do right now is take a deep breath and tell no one. Not your mom, not your best friend, not your boss. This initial “silent period” is your most valuable asset. Discover the best info about macau 5d.

This quiet time creates the space you need to think. Once news gets out, your life changes instantly. As lottery officials often see, winners are overwhelmed with requests from long-lost relatives and strangers, making rational decisions nearly impossible. Financial experts agree that many of the biggest mistakes lottery winners make happen in the first few weeks, born from emotion and outside pressure.

So, who should get that first critical call? The answer is a vetted attorney who has experience with large financial windfalls. This is the crucial first step in understanding what to do after winning the lottery in Virginia. Your lawyer acts as a gatekeeper and helps you assemble the rest of your team, which includes finding a financial advisor for lottery winners who will protect your newfound wealth for a lifetime.

How to Make Your Winning Ticket Legally Yours: 3 Immediate Steps

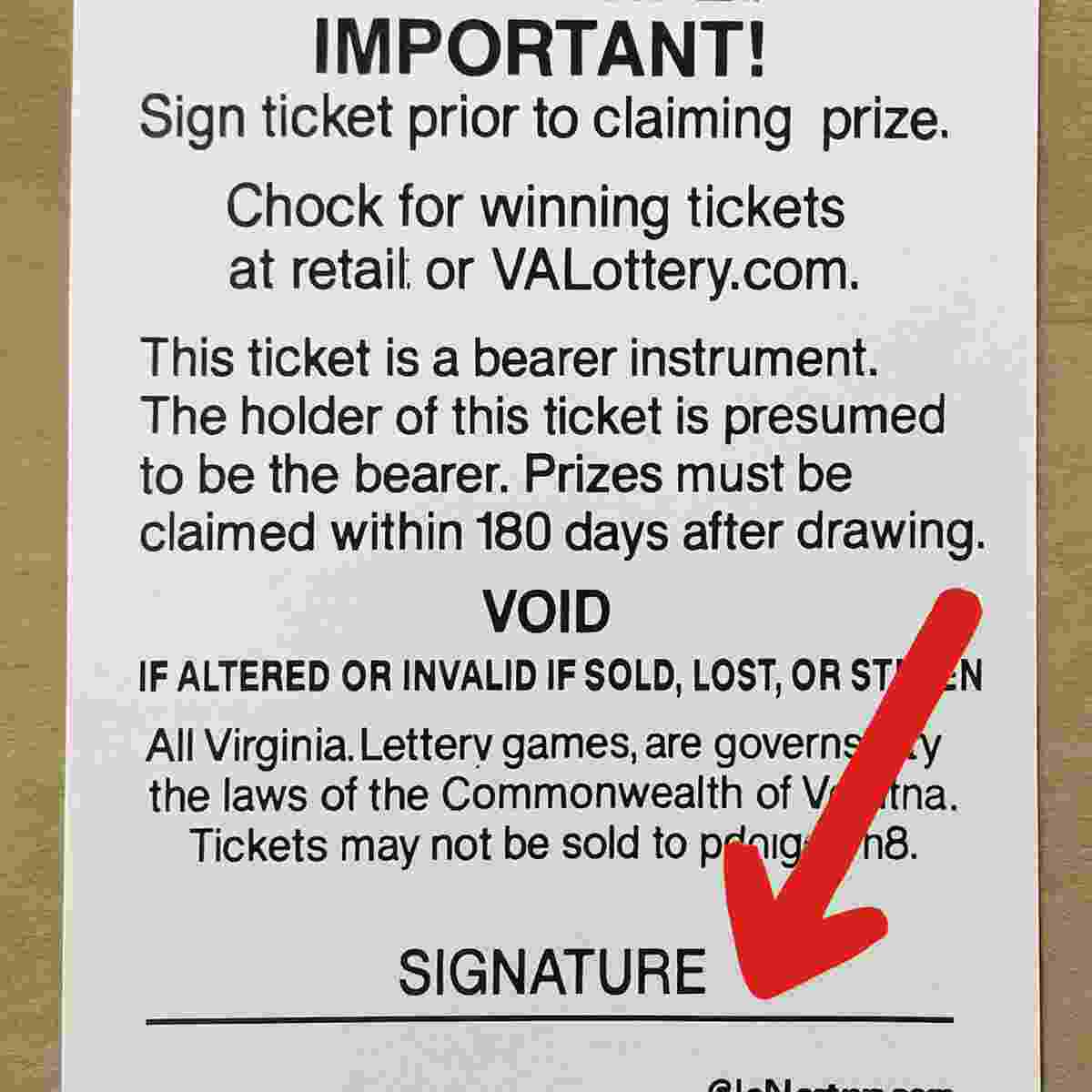

Before you even think about quitting your job or buying a new car, your most critical mission is to protect that small piece of paper in your hand. An unsigned lottery ticket is what’s known as a “bearer instrument”—think of it like cash. Whoever is holding it can claim it. The moment you sign the back, however, it transforms into a legal document that belongs only to you. This simple act is the first line of defense between you and losing everything.

To make that ticket legally and indisputably yours, Virginia Lottery officials and financial experts recommend following three immediate steps before telling another soul:

- Sign the back of the ticket immediately. Use a pen and write your full legal name clearly. This is non-negotiable.

- Document your ownership. Take a clear photo and video of yourself with the front and back of the signed ticket. Save these files to a secure cloud service.

- Secure the physical ticket. Place it in a waterproof bag and store it somewhere incredibly safe, like a home safe or, even better, a bank’s safe deposit box.

These steps might seem basic, but they create an ironclad trail of ownership that protects you from loss, theft, or any potential disputes down the road. With the ticket itself physically and legally secured, you have bought yourself the most valuable asset of all: time. Now you can take a deep breath and begin the next crucial phase without panicking—building the expert team you’ll need before you walk into any lottery office.

Why You Need a ‘Financial Trinity’ Before Claiming Your Prize

With your ticket secured, you must resist the powerful urge to rush to the lottery office. Financial experts universally agree that the next step isn’t claiming the cash, but hiring professional help. Think of it as assembling your personal “Financial Trinity”—a specialized lawyer, a Certified Public Accountant (CPA), and a financial advisor. This team is the single most important investment you can make, creating a buffer between you and a world of sudden, overwhelming complexity.

Your first call should be to a lawyer who has experience with large financial windfalls like lottery wins. This person acts as your shield and strategist. In Virginia, where major jackpot winners can remain anonymous, a lawyer is crucial for setting up the legal structure, like a trust, that allows you to claim the prize without your name being made public. They also serve as a gatekeeper, professionally managing the inevitable flood of requests and protecting you from scams.

Next, the CPA and financial advisor tackle the money itself. The CPA is your tax expert, focused on minimizing the immediate, massive tax bill you’ll face and planning for future tax obligations so there are never any costly surprises. The financial advisor, on the other hand, is your long-term wealth coach. Their job is to create a comprehensive plan to invest your winnings wisely, ensuring the money not only lasts your lifetime but can grow to support your family for generations.

This team isn’t an expense; it’s an insurance policy for your future peace of mind. They work in concert to build a fortress around your new fortune, giving you the breathing room and expert advice needed to make smart choices instead of emotional ones. With their guidance in place, you’ll be fully prepared to face the first major decision every winner must make.

The $100 Million Question: Lump Sum or Annuity Payout in Virginia?

With your team of advisors ready, you’ll face the first monumental choice in your journey as a Virginia lottery winner: how do you want your money? The advertised jackpot amount, say $100 million, isn’t a single check you can cash. Instead, it represents two very different paths you can take, and your decision between the lump sum vs. the annuity payout will shape your financial future from day one.

The first option is the lump sum, also known as the cash value. This is a smaller, single payment of the prize money right now. For that $100 million jackpot, the lump sum might be around $55 million (before taxes). The major benefit is control; the money is all yours immediately, ready to be invested by your financial team for potentially greater growth. The trade-off, however, is that you are accepting a significantly smaller amount than the advertised prize.

Alternatively, you could choose the annuity payout. This option delivers the full $100 million jackpot, but it’s paid out over 30 years. Think of it as a guaranteed, multi-million dollar paycheck from the Virginia Lottery every year, with each payment increasing slightly to help offset inflation. The annuity provides incredible financial discipline and a steady, predictable income stream for decades, but you sacrifice immediate access to the entire fortune.

Ultimately, this decision isn’t about which choice is better, but which one is better for you. It’s a question of control versus security, a conversation you’ll have in-depth with your new financial team. No matter which path you choose, however, one thing is certain: a large portion of that money is already spoken for, which brings us to the next critical reality.

The Tax Man Cometh: How Much of Your Virginia Lottery Winnings Will You Actually Keep?

Whether you’ve chosen the lump sum or the annuity, the next step is unavoidable: taxes. Before a single dollar of that massive jackpot reaches your bank account, the Virginia Lottery is required by law to withhold a significant portion. For any prize of this size, you can expect an immediate 24% deduction for federal taxes and an additional 4% for Virginia state taxes. This initial 28% cut is the government’s down payment, but it’s not the end of the story.

Crucially, this automatic withholding is not your final tax bill. A multi-million dollar prize instantly catapults you into the highest federal income tax bracket, which is currently 37%. This means that when you file your taxes the following April, you will owe the difference between the 24% that was withheld and the full 37% you’re liable for. This future tax payment will be a multi-million dollar event in itself, a reality your CPA will help you prepare for from day one.

These two tax hits—one federal, one state—are completely separate. The federal taxes you pay support national programs, while the Virginia state tax funds everything from local schools to road maintenance right here in the Commonwealth. It’s a financial one-two punch that many first-time winners don’t see coming, which is why having an expert team is so important.

So, how much should you realistically expect to keep? To avoid future shock, financial advisors offer a simple rule of thumb: take your pre-tax winnings and mentally cut them in half. For a $55 million lump sum, this means planning your future around a take-home amount closer to $30 million. With this grounded figure in your mind, you’re ready to navigate the official steps of receiving your life-changing prize.

How to Officially Claim Your Mega Millions Prize in Virginia

With a grounded financial outlook, the next step is to make your winnings official. But don’t wait too long—the clock starts ticking the moment the winning numbers are drawn. In Virginia, you have exactly 180 days to claim a Mega Millions prize. This is a non-negotiable deadline. If you show up on day 181, that life-changing ticket unfortunately becomes just a piece of paper. This strict rule is why experts urge winners to contact their legal team and secure the ticket immediately.

Unlike a smaller prize you could cash at a local retailer, you can’t claim a jackpot at just any lottery office. For any prize over $1 million, the process is centralized at one specific location: the Virginia Lottery Headquarters in Richmond. This isn’t a walk-in service; your lawyer will coordinate directly with lottery officials to schedule a private appointment, ensuring the entire event is handled securely and professionally from start to finish.

When the day of your appointment arrives, the process is surprisingly straightforward. You must bring two essential items:

- The original, signed winning ticket.

- A valid, government-issued photo ID (like a driver’s license or passport).

Lottery officials will verify the ticket and guide you through the final paperwork to begin the transfer of funds. This is the moment all the planning pays off, but it’s also where you’ll make another crucial decision, thanks to a welcome change in Virginia law.

The Most Important New Rule for Virginia Winners: How to Claim Anonymously

That crucial decision is whether you want the world to know your name. For years, the stories of Virginia lottery winners were public knowledge, a requirement that often led to unwanted attention and stress. But a major law change in 2019 gives winners a powerful tool for protection. If your prize is $10 million or more, you now have the legal right to remain completely anonymous.

The reason this change is so significant comes down to two things: safety and sanity. Without anonymity, a winner’s life can be turned upside down by a flood of requests from distant relatives, fake charities, and outright scammers. Publicizing your identity is one of the biggest mistakes past lottery winners make, as it can put a target on your back. Choosing to stay private is the single best step you can take to protect your family and your peace of mind.

Opting for anonymity isn’t automatic, however. It’s a choice you must formally declare when you claim your prize. During your private appointment at the Richmond headquarters, you—or more likely, your lawyer on your behalf—will explicitly state that you are exercising your right to anonymity under Virginia law. Lottery officials will then ensure your name and identifying details are kept out of all public announcements.

Choosing to stay out of the spotlight provides a critical shield from the initial chaos of winning. It allows you to adjust to your new life quietly and on your own terms. While personal anonymity is your first line of defense, many winners take their privacy and financial strategy a step further, which raises another important question.

Should You Claim Your Prize in a Trust? A Plain-English Guide

While personal anonymity keeps your name out of the headlines, creating a trust for lottery winnings provides an even stronger layer of financial privacy. Think of a trust as a legal treasure chest for your prize money. You work with a lawyer to create this “chest” and write a clear set of instructions for how the money inside can be used. This is a common strategy recommended by any good financial advisor for lottery winners.

Putting this plan into action is surprisingly straightforward. Your lawyer can create a trust with a generic name, like “The Blue Ridge Mountain Trust.” Then, the trust itself—not you personally—is what officially claims the prize. This adds another buffer between your identity and the money. When you go to buy a house or make a large investment, the purchase is made by the trust, keeping your name out of public records and away from prying eyes.

Beyond immediate privacy, a trust is also one of the most powerful tools for planning for your family’s future, a process known as estate planning. The instructions you write for your trust can dictate exactly how your winnings are managed and distributed to your loved ones if something happens to you, often without the delays and public nature of going through court. It ensures your legacy is protected according to your wishes.

By setting up this legal and financial foundation, you move from just being a person with a winning ticket to the director of a well-run financial operation. This structure is the key to managing your new reality and is the single best defense for Virgina lottery jackpot claimants against the common mistakes that can lead to the infamous “lottery curse.”

How to Avoid the ‘Lottery Curse’: 3 Common Mistakes New Winners Make

Stories of lottery winners going broke are common, but the infamous “lottery curse” isn’t about bad luck—it’s about predictable mistakes. Having a solid legal and financial foundation is your best defense. Avoiding the curse means steering clear of a few surprisingly simple, yet powerful, human impulses that can quickly derail your newfound fortune.

The most immediate challenge is managing the expectations of family and friends. The emotional pressure to say “yes” to every request for help is immense, but it’s the fastest way to drain your winnings. Your first rule must be The Gatekeeper Rule. When asked for money, use this polite and firm script: “I really appreciate you coming to me. I’ve promised my family and my team that all requests have to go through my financial advisor to ensure everyone is treated fairly.” This creates a professional buffer and protects your relationships.

Next, you must resist the urge to change everything immediately. While buying a mansion or a fleet of cars sounds like fun, rapid lifestyle inflation is what sinks most winners. Institute The 6-Month Rule: Make no major purchases or life-changing decisions for at least six months. This cooling-off period gives you and your team time to create a real plan and lets the initial emotional high settle down.

Finally, many winners fail because they treat their jackpot as an endless pile of cash rather than a business. The solution is The ‘Pay Yourself First’ Rule. Work with your advisor to create a comprehensive budget and pay yourself a generous but structured monthly or annual “salary” from your investments. This simple move from a lottery winner into a well-compensated CEO of your own life is the key to making the money last. These rules are the foundation of your new full-time job: managing your wealth for a lifetime of security.

Your New Full-Time Job: A 3-Phase Plan for Lifelong Wealth

Winning the lottery moves from a chaotic fantasy to a manageable reality when you have a clear plan. The journey begins with one immediate priority: Secure. This means signing that ticket, staying quiet, and assembling the expert team who will act as your shield. This first stage is the foundation for your entire financial future, helping you avoid the most common mistakes lottery winners make.

Once secure, you can shift to Strategize and Sustain. With your team, you will navigate the big decisions—lump sum or annuity, taxes, and claiming your prize privately. From there, you will build the systems to sustain that wealth through careful budgeting and planning, answering the long-term question of what to do after winning the lottery.

Winning isn’t retirement; it’s a promotion. Your new full-time job is being the careful steward of your family’s security for generations to come. By following this path, you trade the anxiety of sudden wealth for the profound peace of mind that comes from being in control. You’re no longer just dreaming of winning—you’re prepared to manage it.