Driving without insurance in Ontario is a serious offense. It carries significant legal and financial consequences. Understanding these penalties is crucial for all drivers. To learn more, check out https://www.trafficparalegalservices.com/no-insurance/

Ontario law mandates car insurance for every vehicle on the road. This requirement is not just a formality. It protects drivers, passengers, and pedestrians.

The minimum fine for driving without insurance in Ontario is steep. It starts at $5,000 for a first offense. Repeat offenders face even harsher penalties.

Beyond fines, uninsured drivers risk license suspension. This can severely impact daily life and employment. Vehicle impoundment is another possible consequence.

Legal costs add to the financial burden. Court fees and surcharges can quickly accumulate. These costs are often unexpected and overwhelming.

Driving without insurance can also affect future insurance premiums. Insurers may view offenders as high-risk. This can lead to higher rates or denial of coverage.

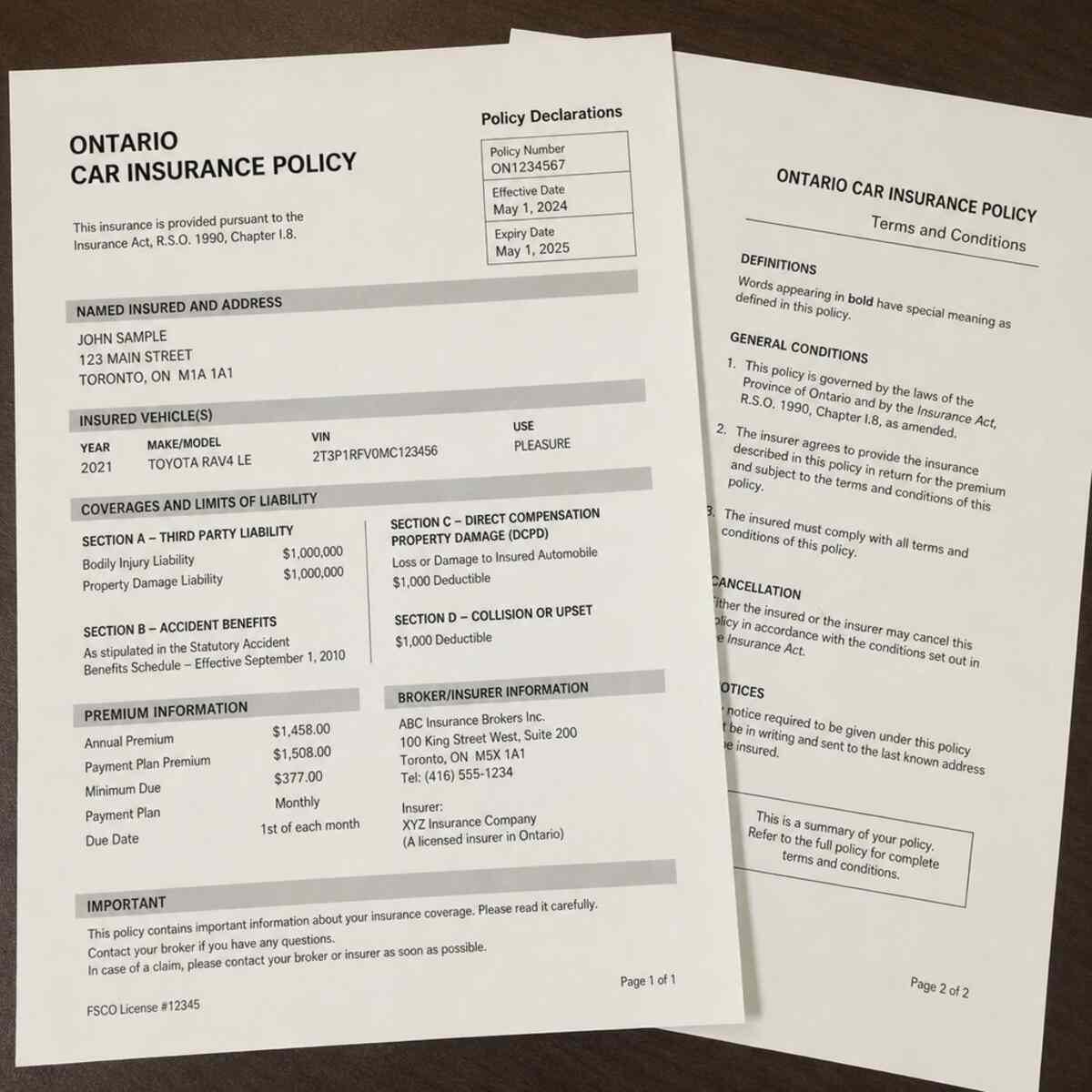

Ontario requires a minimum of $200,000 in third-party liability coverage. This coverage is essential in the event of an accident. Without it, drivers are personally liable for damages.

Uninsured drivers involved in accidents face severe repercussions. They may be sued for damages and injuries. This can lead to financial ruin.

The Financial Services Regulatory Authority of Ontario oversees insurance regulations. They ensure compliance and protect consumers. Understanding their role is important for all drivers.

The Compulsory Automobile Insurance Act enforces these requirements. It is a key piece of legislation in Ontario. Familiarity with this law is essential.

Driving without insurance can also result in a criminal record. This can impact future opportunities. It is a consequence that extends beyond the road.

Legal representation may be necessary for those charged. Navigating the legal system can be complex. Professional advice is often invaluable.

Staying informed about Ontario’s car insurance laws is crucial. It helps avoid legal troubles and financial strain. Knowledge is the best defense against uninsured driving penalties.

Understanding Ontario Car Insurance Requirements

Ontario requires all drivers to maintain valid car insurance. This mandate ensures that drivers can cover accident-related damages. It is a legal and financial safeguard.

The essential component of Ontario car insurance is third-party liability coverage. This coverage protects against injury and damage claims. The minimum required amount is $200,000.

Many drivers choose to buy additional coverage. This can include accident benefits and uninsured motorist protection. Extra coverage provides greater financial security in the event of an accident.

Here’s a quick rundown of what Ontario car insurance must cover:

- Third-party liability: Minimum $200,000

- Accident benefits: Medical, rehabilitation, and income replacement

- Direct compensation: Covers your car in accidents not your fault

- Uninsured motorist coverage: Protects if the other driver lacks insurance

Understanding the various types of coverage is key. Each serves a distinct purpose and offers a distinct benefit. Discuss options with an insurance broker to tailor coverage to your needs.

A common mistake is assuming that comprehensive or collision coverage replaces liability coverage. These cover optional extras, such as vehicle damage from theft or accidents. Liability remains the core legal requirement.

Insurance costs can vary based on several factors. Driving history, vehicle type, and location all influence premiums. Safe driving records generally lead to lower rates.

Review your policy regularly to ensure it meets your needs. Life changes may affect coverage requirements and premiums. Being proactive helps maintain adequate protection.

Adequate insurance coverage is critical for legal compliance and financial safety. It spares you from significant penalties and liabilities. Staying informed can help you make the best decisions regarding your car insurance.

The Compulsory Automobile Insurance Act: What the Law Says

The Compulsory Automobile Insurance Act is fundamental in Ontario. It mandates insurance for all vehicles driven in the province. This law seeks to protect both drivers and victims in accidents.

The Act requires that drivers hold valid auto insurance at all times. Failure to comply can result in severe penalties. It is not just an administrative requirement; it is a legal obligation.

Here’s what the Act dictates:

- Every vehicle must be insured.

- Insurance coverage must include third-party liability.

- Drivers must provide proof of insurance upon request.

- Uninsured driving incurs heavy fines and penalties.

Penalties serve as a deterrent for uninsured driving. The minimum fine for a first offense is $5,000. Repeat offenses see significantly higher fines.

Additionally, driving without insurance can lead to license suspension. This suspension affects your ability to drive and earn a livelihood. Vehicle impoundment may also follow uninsured driving violations.

The law also permits the imposition of surcharges. Courts may impose administrative costs in addition to fines. These financial penalties emphasize the seriousness of the offense.

Compulsory insurance ensures financial restitution for accident victims. It shields individuals from having to bear the entire financial burden alone. It also aids public safety by discouraging uninsured drivers.

The Financial Services Regulatory Authority of Ontario enforces the Act. This regulatory body ensures compliance and protects consumer interests. They oversee insurance operations within the province.

Understanding the Compulsory Automobile Insurance Act is crucial. It informs drivers of their legal responsibilities and consequences. Knowledge of the law safeguards against inadvertent offenses.

Fines and Financial Penalties for Driving Without Insurance in Ontario

Driving without insurance in Ontario incurs severe financial penalties. These fines serve as a stern warning to all drivers. The deterrent effect is intentional and necessary.

First-time offenders face substantial fines. The minimum fine begins at $5,000. This substantial amount underscores the seriousness of the infraction.

For subsequent offenses, the fines escalate. Penalties can reach as high as $25,000. The financial burden increases with each repeat offense.

Additional surcharges often accompany fines. These surcharges include a mandatory Victim Fine Surcharge. This fee helps support victims of accidents.

Here is a list of potential financial penalties:

- Initial offense fine: $5,000 minimum

- Repeat offense fine: Up to $25,000

- Victim Fine Surcharge: Variable amount

Beyond fines, court costs may apply. Legal proceedings carry their own set of fees. Convictions bring a combination of financial responsibilities.

The ramifications on personal finances can be substantial. Payment plans might be necessary due to the size of fines. This financial strain affects household budgets.

Impact on insurance premiums is another consideration. Convictions for uninsured driving almost always lead to higher rates. Insurance companies view these offenses unfavorably.

High-risk drivers face significant premium increases. Insurers might classify these drivers as risky investments. This translates to higher costs for future coverage.

In severe cases, insurance coverage can be denied. Finding a willing insurer may become challenging. This is especially true for individuals with multiple convictions.

Here’s a summary of the potential financial impact:

- Higher insurance premiums

- Challenges in obtaining future coverage

- Potential denial of insurance

Comprehending these financial consequences emphasizes the importance of insurance. The penalties serve as a financial wake-up call for offenders. Without insurance, financial stability can be severely disrupted.

Additional Legal Consequences: License Suspension, Vehicle Impoundment, and Court Costs

Driving without insurance in Ontario carries more than just financial penalties. Legal consequences can also be severe. Ignoring these can result in lasting impacts.

One significant consequence is license suspension. A conviction for uninsured driving often leads to a suspended license. This makes it illegal to drive until reinstatement.

The length of the suspension varies. It depends on the nature and frequency of the offense. For some, this can mean months off the road.

Another serious penalty is vehicle impoundment. Law enforcement can seize the vehicle of uninsured drivers. This impoundment adds to the inconvenience and expense.

During the impoundment period, drivers cannot access their vehicles. Retrieving the vehicle requires paying impoundment and storage fees. This can further strain personal finances.

Here are the key legal consequences:

- License suspension for uninsured driving

- Vehicle impoundment for repeated offenses

Court costs compound the financial burden. Court appearances are mandatory for offenders. These proceedings come with associated fees.

Legal representation might be necessary during court appearances. Hiring a lawyer can be costly but beneficial. This adds to the already mounting expenses.

Court-imposed penalties might include community service. Judges can require offenders to complete specific hours. This serves as a corrective measure in addition to financial penalties.

Additional mandated actions may include driver training courses. These courses educate drivers on insurance requirements. Completing them may be a condition for the reinstatement of driving privileges.

Facing legal consequences requires understanding all potential outcomes. Seeking legal advice is often beneficial. Lawyers can help navigate court proceedings and minimize penalties.

The weight of these legal consequences underscores the seriousness of driving uninsured. Licenses and vehicles are hard-earned and costly to lose. Compliance with Ontario’s insurance laws is non-negotiable for maintaining driving privileges and avoiding substantial legal repercussions.

Criminal and Civil Liability: What Happens After an Accident Without Insurance

Accidents happen, often unexpectedly. Driving uninsured amplifies the risks when involved in a collision. It introduces criminal and civil repercussions.

Criminal liability arises from driving without required coverage. Serious charges may be laid against uninsured drivers after an accident. These charges could lead to significant fines or jail time.

In addition to criminal consequences, civil liability looms. Without insurance, drivers bear full responsibility for damages. This includes vehicle damage and medical costs for injuries.

Victims may pursue civil lawsuits to recover costs. These legal actions can be financially devastating. Court judgments may demand substantial compensation from the uninsured driver.

The Financial Services Regulatory Authority of Ontario (FSRA) plays a role. They oversee insurance compliance and may impose further penalties. It’s essential to understand the gravity of their enforcement powers.

An uninsured accident could lead to the following liabilities:

- Criminal charges due to a lack of insurance

- Civil lawsuits from other parties involved

- Full financial responsibility for all accident-related costs

Criminal records can result from these incidents. Such records affect future employability. Employers often assess candidates’ legal histories during hiring.

The stress of legal battles is significant. Uninsured drivers face financial ruin and emotional turmoil. Legal representation is advisable to navigate these challenges.

Legal guidance helps manage liabilities effectively. Lawyers interpret complex laws and offer strategic advice. This assistance is critical in minimizing potential damage.

Understanding these liabilities highlights the need for insurance. Protection extends beyond compliance—it safeguards against unforeseen accidents. Taking proactive measures to maintain valid insurance is crucial.

Driving uninsured isn’t merely a risk—it’s a costly mistake. Both criminal and civil liabilities serve as a grim reminder. Insurance isn’t just a legal requirement; it’s a vital personal safeguard.

Impact on Future Insurance and Personal Finances

Driving uninsured has profound implications for future insurance costs. Insurance providers view this as a red flag. A record of uninsured driving signals a high risk to insurers.

This increased risk often results in premium hikes. Insurers may charge far more for coverage. In some cases, finding affordable insurance becomes extremely challenging.

Individuals may experience outright denial of coverage. Some providers refuse to insure those with a history of uninsured driving. This leaves fewer options for consumers.

Financial penalties further burden individuals. Fines and legal costs from uninsured accidents add up quickly. These expenses strain personal finances significantly.

Uninsured driving might affect your credit score. Financial judgments can lead to unfavorable credit reports. Poor credit impacts various facets of life, beyond insurance.

Employment prospects could suffer due to financial instability. Certain employers assess credit scores and financial history in hiring decisions. Stability concerns could hinder job opportunities.

Bankruptcy is a potential risk for some. Accumulating debts from lawsuits and fines contribute to financial distress. Extreme cases may lead to filing for bankruptcy protection.

Considering these impacts, maintaining insurance is crucial. Avoiding lapses saves money and stress down the line. Here’s what you can anticipate if caught driving uninsured:

- Higher insurance premiums or refusal of coverage

- Significant financial penalties and fines

- Negative impact on credit score

Balancing these risks against insurance costs highlights the value of coverage. Insurance provides peace of mind and shields you from financial disaster. Staying insured is not just legal compliance; it’s smart financial planning.

How Driving Without Insurance Affects Employment and Criminal Records

Driving without insurance in Ontario has repercussions beyond financial ones. Legal issues can impact your employment prospects. Many employers conduct background checks, especially for roles involving company vehicles.

A conviction for uninsured driving can appear on these checks. Employers may view this as a reflection of responsibility. It could affect your chances of being hired or promoted.

In roles that require a clean driving history, this is especially concerning. Professional drivers, such as delivery personnel or truck drivers, face stricter scrutiny. An uninsured driving record might disqualify candidates outright.

Moreover, some positions require a valid driver’s license. Legal penalties for uninsured driving can include suspension. This poses an immediate hurdle for jobs that demand active driving.

Criminal records can haunt job applications. Although driving uninsured is not always a criminal offence, in severe cases it may involve additional legal concerns. Repeat offenses could exacerbate this issue.

Here are some potential consequences on employment:

- Difficulty securing jobs requiring clean driving records

- Challenges in roles needing valid driver’s licenses

- Negative impact on background checks, affecting job offers

Furthermore, having a legal record can limit your career growth. Promotions and new opportunities may become elusive. Employers prefer candidates without such complications.

Reflect on the broader implications of failing to comply with insurance laws. It extends beyond legal penalties to areas such as career advancement and job security. Being uninsured risks more than just fines; it jeopardizes future professional opportunities. Guarding against this by maintaining proper insurance is a wise decision.

The Role of Insurance Companies and Regulatory Bodies in Ontario

Insurance companies and regulatory bodies are crucial in maintaining order in Ontario’s insurance landscape. They ensure drivers comply with legal requirements and provide necessary coverage options.

The Financial Services Regulatory Authority of Ontario (FSRA) regulates the province’s insurance sector. Their job is to ensure fair practices and protect consumer interests. They set the standards for the industry and enforce legal requirements.

Insurance companies offer various coverage plans to fit diverse needs and budgets. They perform risk assessments to determine premiums, considering factors like driving history and vehicle type. This individualized approach aims to balance coverage affordability and protection.

Both insurance providers and regulatory bodies focus on consumer education. They publish resources to inform drivers about their rights and responsibilities. This fosters informed decision-making when selecting coverage plans.

Key roles and responsibilities include:

- Regulating insurance practices to ensure fairness

- Offering coverage options tailored to consumers’ needs

- Educating the public on insurance requirements and rights

For drivers, understanding the involvement of these entities is essential. A well-informed consumer can navigate the insurance landscape effectively. This awareness also aids in recognizing and reporting unfair practices.

In Ontario, the collaboration between insurance firms and regulatory bodies safeguards drivers’ interests. By maintaining transparency and enforcing regulations, they contribute to the overall stability of the insurance market. This system ensures that all parties involved abide by established laws, promoting safer roads and responsible driving behaviors.

How to Check and Prove Your Insurance Status in Ontario

Knowing your insurance status is crucial as a responsible driver in Ontario. It ensures you’re compliant with legal requirements and protected on the road.

To verify your insurance, first check your insurance policy documents. These documents contain all the details about your coverage, including the insurer, policy number, and coverage terms. Keep them accessible for reference.

You can also contact your insurance provider directly. They can confirm the status and details of your policy over the phone or through an online account. This method provides immediate assurance and clarification of your coverage.

Proof of insurance is mandatory when driving in Ontario. You must keep an insurance card in your vehicle. This card includes key information like:

- Insurance company name

- Policy number

- Vehicle description

- Coverage validity dates

In case of a police stop or after an accident, this card is your proof of current insurance.

Additionally, use digital options such as mobile apps that many insurers offer. These apps often feature electronic insurance cards, making it convenient to show proof when needed.

Always ensure your insurance information is up to date, especially after changes such as switching vehicles or insurers. In Ontario, driving without proper documentation or coverage can lead to severe penalties.

Maintaining up-to-date insurance records and proof of insurance will help you avoid legal complications. This practice contributes to smoother interactions with law enforcement and ensures peace of mind while on the road.

Types of Car Insurance Coverage in Ontario: What You Need to Know

In Ontario, understanding the different types of car insurance is essential for making informed decisions. The right coverage protects you and your vehicle from unforeseen events.

Every driver must have third-party liability insurance. This mandatory coverage protects against costs from injuries or damages you cause to others. Ontario law requires a minimum coverage of $200,000, but higher limits are advisable.

Accident benefits coverage is another key component. It covers medical expenses and income replacement if you’re injured in a car accident, regardless of fault. This safeguard ensures you receive the necessary care and financial support.

Uninsured motorist coverage protects you if an at-fault driver lacks insurance or if you’re involved in a hit-and-run. It covers damages to you and your passengers, ensuring you’re not left without assistance.

- Third-party liability

- Accident benefits

- Uninsured motorist

Consider comprehensive insurance for broader protection. It covers theft, vandalism, and non-collision damage, such as damage from natural disasters. While optional, this coverage adds significant peace of mind.

Collision insurance handles repair costs for your vehicle following an accident, regardless of fault. It’s particularly important for newer vehicles, as it helps manage potential repair costs.

- Comprehensive coverage

- Collision coverage

Optional additional endorsements can enhance your policy. These include options like rental car coverage or forgiveness for a first accident. Endorsements personalize your insurance to fit unique needs.

Choosing the right balance of coverage is crucial. Assessing your vehicle’s value, lifestyle, and budget aids in selecting appropriate insurance types.

Regularly review and update your policy to align with any changes in your circumstances. Staying informed empowers you to make decisions that best protect your interests and comply with Ontario’s car insurance laws.

What to Do If You’re Charged With Driving Without Insurance

Facing a charge for driving without insurance is a daunting experience. Understanding the steps to take can help mitigate the situation.

First, remain calm and collect all relevant documents. This includes your vehicle registration, insurance papers (if applicable), and identification.

Next, consider seeking legal advice. A lawyer can provide guidance on how to navigate the legal process. They may help reduce potential penalties or explore possible defenses.

Prepare for your court appearance meticulously. Understand the charges against you and the potential consequences. Being well-prepared demonstrates responsibility and may positively influence the outcome.

During court proceedings, present any mitigating circumstances. If you were unaware your policy lapsed, or there were other extenuating conditions, communicate these clearly.

- Gather essential documents

- Seek legal counsel

- Prepare for court

- Communicate mitigating factors

Understanding the possible penalties is vital. Fines can range from $5,000 to $25,000 for repeat offenses. A conviction may also result in a driver’s license suspension and increased insurance premiums.

If found guilty, comply with all penalties promptly. Meet any requirements to reinstate your license and address any surcharges. Compliance is crucial for minimizing future complications.

Maintaining open communication with your insurance company is beneficial. They can guide you on steps to prevent future lapses and explore options for future coverage.

Learning from this experience is paramount. Ensure your vehicle is continuously insured to prevent future legal issues. Proactivity and diligence now can safeguard against further consequences down the road.

Reinstating Your License and Insurance After a Conviction

After a conviction for driving without insurance, reinstating your license becomes a top priority. The process often involves several steps and interactions with various agencies.

First, fulfill any court-mandated requirements. This typically involves paying fines and serving any suspension periods. Delay in compliance can prolong the reinstatement process.

Next, contact the Ministry of Transportation, Ontario (MTO). They provide guidance on the necessary steps and documents needed for license reinstatement. It’s important to follow their instructions closely.

Rebuilding your insurance record is another critical step. Approach multiple insurance providers to discuss your situation. A conviction can make this process challenging, but it’s essential for legal driving.

Some insurance companies may offer options like high-risk insurance policies. Though expensive, they may be necessary in the short term. Regularly review your policy to find more affordable options over time.

- Complete court requirements

- Consult with MTO for license guidance

- Explore high-risk insurance options

Documentation is key. Keep all related paperwork organized and readily accessible. This ensures quick reference and smoother interactions with authorities.

Restoring your driving privileges and insurance requires diligence. The process may be long, but persistence and adherence to legal requirements are crucial. Show responsibility in maintaining insurance, and your record could improve over time.

Strategies for Finding Affordable Ontario Car Insurance

Finding affordable car insurance in Ontario can seem daunting, but strategic approaches can make the process easier. It’s all about knowing where to look and what to consider.

Start by comparing quotes from multiple insurers. Many online platforms allow you to input your details and receive estimates from various companies. This makes it easier to identify competitive rates.

Consider bundling your insurance policies. Insurers often offer discounts if you purchase multiple types of insurance from them. Combining auto and home insurance, for instance, might yield savings.

Raising your deductible is another option. A higher deductible generally reduces premium costs. However, ensure you can afford the deductible if an accident occurs.

- Compare quotes from several insurers

- Consider bundling insurance policies for discounts

Enroll in a driver’s education course. Some insurers offer discounts to drivers who complete these programs. It shows a commitment to responsible driving, often reflected in lower premiums.

Maintain a clean driving record. Traffic violations and accidents can hike insurance costs. Drive safely to avoid surcharges on your premiums.

- Raise your deductible for lower premiums

- Complete driver’s education courses for discounts

Participate in usage-based insurance programs. These involve installing a device in your vehicle that monitors driving habits. Safe driving could lead to significant premium reductions.

Lastly, regularly review and adjust your coverage. Over time, your needs may change. It’s wise to reassess your policy periodically to ensure it still suits your requirements.

By taking proactive steps, you can effectively manage your car insurance expenses in Ontario.

The Broader Impact: Uninsured Driving and Public Safety in Ontario

Driving without insurance doesn’t just affect those involved; it impacts broader public safety in Ontario. Every driver on the road is at potential risk due to uninsured drivers.

Uninsured vehicles compromise financial safety for law-abiding citizens. In an accident, insured drivers might incur unreimbursed expenses, increasing their personal financial burdens.

Public resources are stretched by uninsured driving incidents. Emergency services and judicial resources are often tied up in handling these cases. This diversion affects the timely availability of services for other emergencies.

The repercussions extend to road safety statistics. Uninsured driving incidents can skew data, affecting the province’s road safety initiatives. Accurate data is pivotal for crafting effective safety policies.

- Financial safety of insured drivers is compromised

- Public resources are strained

- Road safety data may be distorted

Community awareness campaigns often highlight the risks of uninsured driving. These endeavors aim to educate drivers about legal obligations and safety responsibilities.

Increasing public awareness and education efforts are vital. By understanding repercussions, drivers may be more inclined to comply with insurance laws. Greater compliance can lead to safer roads and less strain on public resources.

Ultimately, uninsured driving has far-reaching consequences. It stresses the community, distorts safety data, and places financial burdens on others. A collective effort is required to mitigate these impacts and ensure the safety and well-being of all drivers in Ontario.

Frequently Asked Questions About Driving Without Insurance in Ontario

Navigating the landscape of car insurance in Ontario can be daunting. Here are some frequently asked questions that can provide clarity.

What Happens If I Drive Without Insurance in Ontario?

Driving without insurance in Ontario invites serious penalties. The minimum fine is $5,000 for a first offense.

Subsequent offenses can incur fines up to $25,000. Additionally, there may be a license suspension or vehicle impoundment.

How Can I Check If My Car Insurance Is Valid?

Ensure your insurance details are up-to-date. Contact your insurance provider for confirmation. Many insurers also offer online portals for convenient access to your policy details.

What Types of Coverage Are Mandatory in Ontario?

Ontario mandates a minimum of $200,000 in third-party liability coverage. This requirement helps cover damages you may cause to others.

- Minimum $200,000 third-party liability

- Accident benefits coverage

- Uninsured automobile coverage

It’s wise to consider additional coverage based on personal needs, such as collision or comprehensive insurance.

Can I Be Sued for Causing an Accident Without Insurance?

Yes, you can be sued if you cause an accident without insurance. You’ll be personally liable for damages and injuries. Legal fees and court costs can accumulate, adding to the financial burden.

Does Uninsured Driving Affect My Future Insurance Rates?

A conviction of driving without insurance will likely raise future insurance premiums. Insurers consider this high-risk behavior, which can lead to significantly increased rates.

Can I Still Get Insurance After a Conviction?

Yes, but at higher rates. Some insurance companies might refuse coverage altogether. Consulting with a broker can help you explore available options.

- Higher premiums post-conviction

- Some insurers may deny coverage

- Consult brokers for alternatives

Why Is It Important to Have Adequate Insurance?

Insurance ensures financial protection against accidents. It covers potential costs from damages or injuries, safeguarding your assets. It also complies with Ontario’s legal requirements, thereby avoiding hefty fines and penalties.

Conclusion: The Importance of Staying Insured and Informed

Staying insured in Ontario is not just a legal requirement but a crucial responsibility. Driving without insurance poses significant risks to your financial health and legal standing.

The penalties for uninsured driving are severe and far-reaching. Financial burdens from fines and potential lawsuits can be overwhelming. Moreover, the impact on future insurance costs makes compliance with insurance laws imperative.

Having adequate car insurance provides a safety net. It covers unexpected damages and injuries, offering peace of mind. This protection is invaluable in mitigating the unpredictability of driving.

Keeping informed about Ontario’s car insurance requirements helps you make smart insurance decisions. Regularly reviewing your policy ensures it meets legal standards and your personal needs. Educating yourself about insurance options can lead to better, more cost-effective coverage.

Ultimately, maintaining valid car insurance is an investment in your personal security and legal compliance. By prioritizing insurance and staying informed, you shield yourself from potential legal issues and financial distress. This proactive approach supports public safety and ensures that you are prepared for any eventualities on the road.